City Journal: How to End Home-Equity Theft

The Supreme Court’s decision last May in Tyler v. Hennepin County represented a major victory for property rights across the United States. The landmark ruling helped protect homeowners’ equity by declaring it unconstitutional for governments to take more than they are owed when collecting a property-tax debt. In the wake of the ruling, some counties have complained that their gravy train has dried up. Still, there is much work to be done to protect homeowners’ rights.

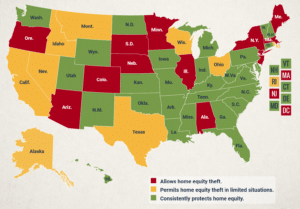

Proponents of homeowners’ rights should support a ban on home-equity theft—a practice whereby the government takes the property of someone who has fallen behind on his taxes and sells the property to cover the debt, pocketing the surplus proceeds. Nineteen states still allow home-equity theft, despite the Supreme Court’s ruling in Tyler that this violates the Takings Clause of the Fifth Amendment. Some states even let private investors buy tax debts and reap the windfall when the taxes go unpaid. Either way, the practice leaves the original owner with nothing.

Fortunately, in recent years, home-equity theft has received broader public attention after successful legal challenges by Pacific Legal Foundation, where I work, and ample media coverage of the practice’s injustice. But supporters of homeowners’ rights should not be complacent. Some states and localities continue these predatory seizures, profiting off vulnerable citizens. Only two states, Nebraska and Maine, have changed their laws post-Tyler.

The story behind the Tyler decision illustrates how abusive these schemes can be. After Geraldine Tyler, a 94-year-old Minnesota grandmother, moved into a senior-living apartment, she missed $2,300 in property-tax payments on her condominium. With penalties and interest, her tax debt ballooned to $15,000. County officials launched tax-forfeiture proceedings, seizing Tyler’s condo and selling it at auction for $40,000. Then the county kept the $25,000 profit rather than returning the excess equity to Geraldine.

I’ve seen scores of home-equity-theft cases in my work as an attorney, and certain patterns have emerged. The homeowners targeted are typically senior citizens living on fixed incomes, people with serious medical or mental-health conditions, or people who have hit a financial rough patch. In most cases, the initial tax amounts owed were relatively small and could have been dispatched through a payment plan. In the most outrageous case, Uri Rafaeli lost his Michigan home when the county seized and sold his property after he mistakenly underpaid his taxes by a mere $8.41.

Those small tax debts add up to significant losses for property owners. A 2022 PLF study estimated that, between 2014 and 2021, U.S. homeowners lost at least 8,600 homes and more than $780 million to home-equity seizures. On average, the homeowners involved lost 86 percent of their equity. That figure constitutes a massive transfer of wealth from struggling American homeowners to government agencies and private investors.

Pacific Legal Foundation has advised policymakers in several states on how to protect homeowners more effectively, and it has published policy guidelines and model legislation to help states end home-equity theft once and for all. Legislation is the only path to complete reform, as it allows the state to revise complex tax-foreclosure procedures to protect homeowners and avoids a costly and protracted legal battle.

Property owners must pay their taxes, of course, and those who fail to do so should face consequences. But in the extreme event that properties are seized or liquidated, the owner’s equity must be returned once the tax debt is settled. As Chief Justice John Roberts wrote in his unanimous Tyler opinion: “The taxpayer must render unto Caesar what is Caesar’s, but no more.”

Those states that persist in stealing homeowners’ equity in the aftermath of the Court’s Tyler decision can expect to face legal action eventually. Meantime, state legislatures should work to make home-equity theft a thing of the past.

This op-ed was originally published at City Journal on January 15, 2024.